- Legal

- Funeral

- Pricing per monthIndividualFamily

- Compare all Individual Plans

- Compare all Family Plans

- Health

- Pricing per monthIndividualFamily

- Compare all family Plans

- Compare all individual Plans

- My AI Lawyer

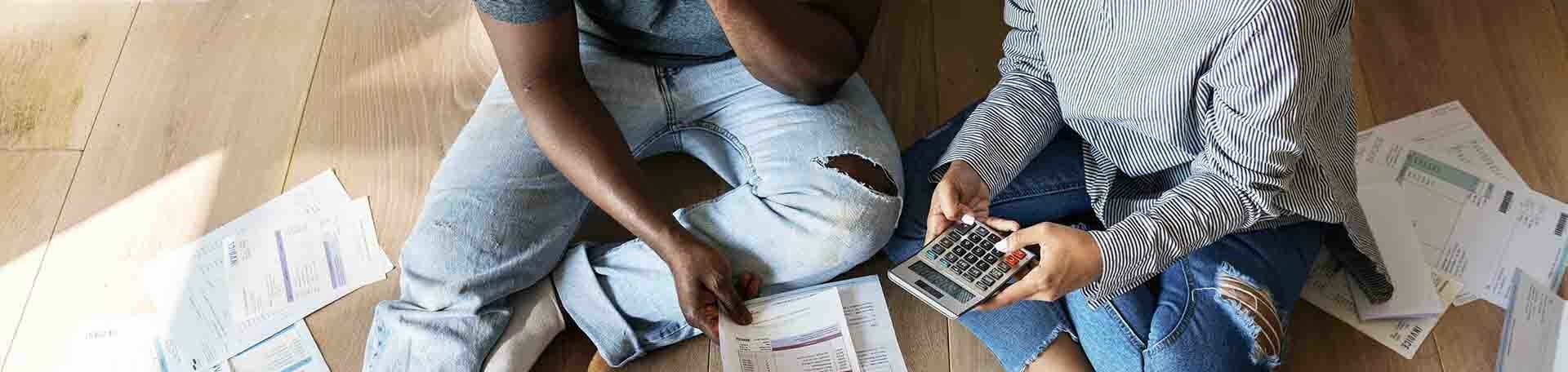

The interest rates of credit agreements and how to better manage your debt

The interest rates of credit agreements and how to better manage your debt

Get the best interest rate to avoid unnecessary additional costs.

The costs of interest can quickly become exorbitant. Read the pros and cons of the different types of interest and avoid any unnecessary debt.

When it comes to credit agreements, interest rates are charged for a period in proportion to the amount borrowed. The total interest is therefore dependent on the principal debt, the interest rate, compounding frequency and length of time borrowed.

Rising interest rates

If the base interest rate rises then the cost of borrowing for commercial banks becomes higher which encourages them to raise their own interest rates. This means that businesses and consumers get higher returns on savings while borrowing becomes more expensive. This lowers economic activity and causes a slow economic growth. Money supply tightens and the demand for goods and services such as food, fuel and lending become more expensive.

How to choose between fixed or variable interest rates

The choice between variable and fixed interest rates is dependent on whether consumers can handle the effect of market forces on their interest rates. Variable interest rates means that interest can go up or down on certain credit agreements depending on the prime market rate determined by the South African Reserve Bank. The prime rate is currently 7.75%. Fixed rates remain the same regardless of fluctuations in the market which guarantees 100% accuracy in budgeting as repayments remain the same and interest on credit agreements are not affected.

Pros and cons of Fixed interest rates

| PROS |

|

| CONS |

|

Options available to over-indebted consumers

In South Africa, over-indebted consumers have debt relief options such as sequestration (The term sequestration is used when the estate of a personwho is no longer able to pay their debts due to uncontrollable circumstances, is surrendered by order of the court). The estate of natural persons, partnerships and trusts can be sequestrated under the Insolvency Act, administration under the Magistrates Court Act and debt review under the National Credit Act.

The National Credit Act protects consumers who enter into credit agreements with independent credit providers and applies to all credit agreements effective or entered into within South Africa. A consumer entering into a credit agreement must carefully read through the terms and conditions of the agreement to ensure that they understand their rights under the agreement. We can assist by reviewing and advising on any agreements on contracts you have in place.

Preparing for the future

How to avoid bad debt?

The best way to avoid pressure from creditors is to ensure that bills are paid on time. Although credit agreements such as mortgage loans, car payments and other loans are virtually a necessity for most consumers today, avoiding overdue bills and minimizing debt is in the best interest of all consumers.

- Pay with cash whenever possible and stay within your spending limits

- Avoid impulsive buying

- Avoid "buy now, pay later", particularly offers that merely postpone debt

- Compare prices before making major purchases

- Avoid borrowing to buy, such as "staple goods" (wheat, sugar, rice, bread and milk)

- If you cannot avoid borrowing, use take the time to find the lender with that will offer you the lowest interest rate and best repayment terms

Calculation methods to help determine your maximum threshold

Once the pros and cons of extending credit to a customer are weighed and the consumer is deemed a good credit risk, the creditor now has to figure out how much credit to offer. This is done in by setting appropriate credit limits which is important to ensure responsible lending by giving the consumer what they need while also protecting the lender against financial instability. There are certain ways in which the lender can determine credit limits which help mitigate the risks of reckless lending.

These methods are as follows:

The net worth method

This method gives you a credit limit based on the customer’s net worth which provides a strong credit limit benchmark based on concrete financial information. This is best done by limiting the credit offered to 10% of the customer’s net worth. This means that the consumer’s financial information is gathered by compiling the customer’s total assets and total liabilities to determine their net worth.

From there you can work the equation:

| Net worth equation = (customer’s total assets -total liabilities) / 10 |

The trade reference method

Trade references are mostly found on credit reports or references provided by the customer on their credit application. This will give you an idea of how much other creditors have already extended credit to the consumer to determine affordability.

The needs-based method

This is calculated based on how much credit the consumer is requesting. This does not mean that credit is offered blindly to the consumer since much consideration of risks are taken into account. In this case, the creditor offers a credit limit based on the consumer’s need to ensure the credit offered does in fact serve its purpose.

Best practice

Although the above credit limit methods are separate, it is commonly accepted practice that all three are used as a starting point to determine a customer’s average credit limit. A credit limit is not set in stone; therefore, a consumer’s credit worthiness is to be assessed and consistently re-evaluated to keep tabs on their financial health.

Want to improve your credit score? Legal&Tax has got you covered with our insightful tips on how to achieve the credit score you need.

Contact us for more information:

Recommended articles

LEGAL&YOU JUNE 2026

This month's newsletter covers youth education opportunities, child protection laws, winter fire safety, and important 2026 tax season dates. Stay informed with practical tips to help protect your family, plan ahead, and navigate key life decisions with confidence.

3 June 2026

Article